If you’ve ever sent money overseas, you’ve used a SWIFT code. That unique identifier ensures money reaches the correct bank and account internationally.

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, was founded in 1973. It doesn’t actually transfer money; instead, it sends secure messages instructing banks to move funds.

Transfers once took one to five business days, but 90% now reach the recipient bank within an hour, according to SWIFT’s 2024 annual review. However, SWIFT’s fees make sending smaller amounts across borders less practical, creating a market for mobile-first remittance fintechs like Mukuru and WorldRemit, which offer cheaper, more accessible alternatives.

SWIFT remains dominant for large, high-value transactions and continues to evolve, most notably through its Global Payments Innovation initiative, which enables real-time end-to-end payment tracking and clearer visibility on transaction costs.

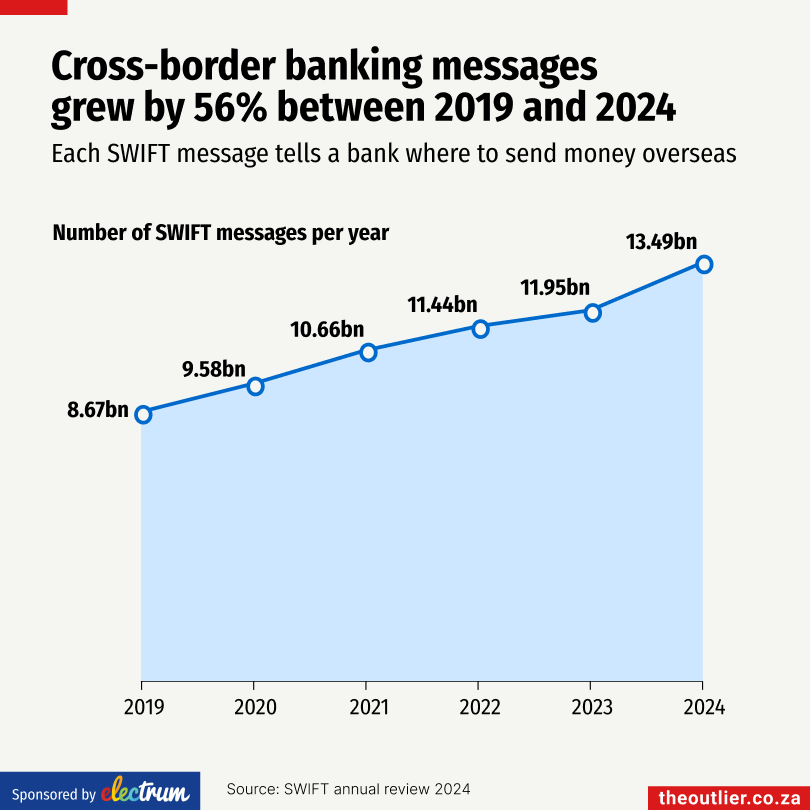

SWIFT message volumes rose from 8.67-billion in 2019 to 13.49-billion in 2024, a 56% increase in five years. As global rails evolve, our latest research predicts a further "disruptive expansion" in the cross-border landscape driven by regional links and tokenised instruments. Download the full South Africa’s Payments Future Report to see how bank leaders can navigate this transition and define the next generation of payments.

Produced by The Outlier in partnership with Electrum, the next-generation payments software company, powering payments for banks and retailers.